Cash Envelopes — a Hands-On Exploration

What Is the Cash Envelopes System?

Cash Envelopes, otherwise known as “envelope budgeting” or the “envelope system” is literally putting your cash in an envelope. Henceforth, I am trying out the cash envelope, because all prior budgeting tactics we have tried have failed miserably. I’ll walk through the cash envelopes system, how I got here, and report back on progress.

How’d We Get to Cash Envelopes?

Like I’ve said, we do OK as a married couple. Not spectacularly rich, but we should be able to save considerably and grow our nest egg and start working meaningfully toward FIRE yada yada yada. But we are not on this track. We invest some in conventional and non-conventional ways but in sum total we’re still in debt, and we’re in the red a lot of months. Part of this is due to deliberate choices: we are investing in primo early childhood education for our two kids. We live in a relatively expensive area in a state with a relatively unfriendly tax code for various reasons.

Still, point is, we should be able to pay down debt and invest bigger chunks of change every month. What’s holding us back?

Here are the major factors, some psychological and some logistical:

Money avoidance: it manifests in different ways in both of us (my wife and I) but in the classic way, we both avoid thinking too seriously about where our money goes or how to do better with it. This compounds because we don’t have productive discussions about how to be better with money.

Down-the-fairway lifestyle creep: neither of us want visible markers of wealth. And yet we keep ratcheting up spending in line with our improvements in household income. Partly this is because we have wealthier friends who we like to have experiences with. Partly it’s just letting our guard down when we should know better… I probably spent $20K more for a new EV than I needed to at the time, for example.

Inflation. We all know about inflation. Fuck inflation. Noteworthy: inflation has been rough for all kinds of people but it’s hurt parents of young kids because childcare and groceries have outpaces other forms of inflation.

Not having a system we can both get behind. When you start a family with someone else you’re trying to reconcile different ways of planning, different emotional postures toward money, different analytic abilities.

I want to talk some about the last point. I’ve read tons of books on personal finance and investing. I’ve read books on behavioral economics and the cognitive biases that keep us doing dumb shit over and over. The common thread: successful personal finance comes down to discipline over a long timeframe, being self-aware, and being cognizant of the lizard brain traps that will undermine you if you aren’t careful.

Aye aye, Mr. Lincoln...

Having a budgeting tool that you can use and that your partner is on board with is critical to making this happen. We’ve tried and failed with a few different systems:

Apps: We were excited about YNAB. Lots of research-backed behavioral tricks and personal finance principles go into this thing. We just couldn’t get comfortable with it. Despite being marketed as a simplifier, there’s a ton of educational content out there just to help you understand what’s going on. There’s a guy who has made a life out of teaching people how to use YNAB… (he even has a whole video on how to rectify a painful mistake that people often make when setting the thing up)... this does not bode well for ease-of-use.

… with the exception of Rocket Money, I’ll get to this in a second

Logging stuff on spreadsheets — my wife refuses to use Google Sheets, so this didn’t work

A fully analog leger — my wife proposed a system of writing things down analog, specifically groceries. Obviously this did not work, for obvious reasons

A system for two people in partnership to manage join finances must be simple and it must have full buy-in of both parties. This is how we got to a souped up version of “envelope budgeting,” the most brain-dead simple method of managing a budget.

You could also just take this advice…

Here’s How Cash Envelopes Works

There might be a more dialed-in way of doing cash envelopes, but having done some research, this is the basic idea. You may want to tweak around the margins to get to the right system for you.

Establish monthly spending budget for all “non-committed” dollars. This begins with an accounting of how much you take in and how much goes out. In other words, anything recurring can go on a credit card (in some cases it has to). This does not make it into your envelope.

Take whatever is left over (the net surplus) and commit whatever you want to, or need to, to saving or paying off debt. This also does not make it into your envelope. You can set up recurring deposits into a savings account, or set up recurring debt repayments.

Make sure you’re accounting for Step 1 in Step 2. In other words, if you’re paying for things like gym memberships or boxes of diapers or whatever with a credit card, make sure that you’re covering that with your debt repayment so that your credit card balance is shrinking by an appropriate target amount each month.

With whatever net surplus is left over after these steps, you literally put that cash into envelopes and use it throughout the month for your discretionary spending. As you’re getting moving with this you’ll want to do a gut check on whether this is a realistic goal or if your monthly recurring commitments (gym memberships, etc.) need to be reconsidered. In practice for me and for most people this will cover groceries, gas, eating out, and occasional luxuries like surf wax or gifts for my kids. You’ll then be doing crude mental math throughout the month. I can spend $X per day, what’s my run rate, and therefore should I buy expensive ramen for lunch or should I bring the leftover mediocre lasagna that my kids didn’t eat but that will be free (and, in fact, avoid food waste and buy me an additional half hour to read or go for a run).

If you have surplus month-to-month (i.e. cash left in your envelope) you can either roll it forward or put it into a separate envelope for “analog savings". Or both. If you have a second cash envelope for savings, probably deposit that into a bank so you can either pay down additional debt or place in a liquid investment vehicle.

This analog method might make you feel like a dumbass caveman! Good. You are a dumbass caveman until you pay off your credit card debt. You are not alone. I have credit card debt. I am a dumbass caveman.

The envelope budgeting method brings you into tangible, tactile contact with the money you are spending. When you pay too much for takeout, you pull that money out, count it, and put your change back into a dwindling stack. As you move through your day, and your weeks, and your month, this method of tracking spending basically turns you into Dave Chappelle on his first date in Half Baked — you’re more aware of what you’re spending, you’re more attuned to what you don’t need, and you ultimately get creative about how to stretch your cash.

(note: Righteous Money does not endorse stealing loose change from the unhoused, or anyone else).

Looking at this from the other angle: buying stuff with credit cards makes you feel rich when you are not, in fact, rich. (Putting this in perspective: if you live in the U.S. and make enough money to actually be thinking about saving it, you are definitely rich in a broader sense, but I digress). Credit card purchases are easy and make you feel like a goddamn money wizard. You never touch the money you spend, so each hit to your credit card feels like nothing until you see a $9K credit card balance and wonder what happened. Now, you may read all this and think “but I get points on my credit card! I have a few for different purposes and I’m benefitting, e.g. Savor Card for restaurants, Amex Blue for gas, etc. etc.” … this is a trick! Rewards are basically how credit card companies trick you into thinking you are doing something financially savvy when in fact you’re being an idiot with your money. You may get (at the high end) something like 5% cash back for a qualifying restaurant purchase. But you’re paying 25%+ APY on your credit card balance… so if you aren’t paying that purchase off every month, you’re actually “earning” a negative 20% annualized on that spending. More importantly, that “rewards” scheme makes you feel like you’re being smart by buying that takeout Thai food (which, by the way, is loaded with sugar and aggressive sodium and transported in sketchy plastic vessels that will sit in a landfill until eternity) when you could have just made some lentils at home.

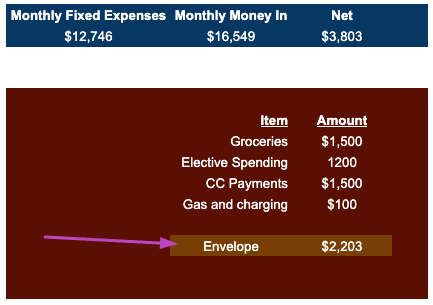

My Cash Envelopes Math

After running through the exercise I delineated above, I arrived at the following figures. The arrangement between my wife and I is that I handle most of the recurring expenses (which are very recurring and very expensive) and she transfers a percentage of her income monthly to help out. Beyond that we’re on our own with discretionary spending. There’s no reason cash envelopes couldn’t work for more tightly coupled finances, however.

So basically I'm grouping in "groceries" with electives like grabbing a beer, taking the kids the science museum, etc. This will not be penny-perfect; using the cash envelopes method you invariably end up using a credit card here and there. I’ve found already, though, that the tangible exercise of pulling cash in and out of the envelope, and watching it leave my hand, has the intended effect of making me think harder about my spending.

You might notice that my “monthly money in” is decently high and my fixed expenses are quite large. This is not because I’m a cocaine addict. As noted, life is expensive now (especially for parents) and we’re investing in early childhood education for our children. What I noticed when really assessing this is just how much we’ve committed to in recurring costs, and how little margin we have for spending, even as a relatively high-earning family. Hence the cash envelopes.

An example: I just spent $19.27 at our local (very cute) grocery store. I got two avocados, some organic burrito wraps, and a single jalepeno. For. Fuck’s. Sake. I now have no more money in my wallet, and will need to return to my cash envelope to re-up. I now have some bias about going back to this cute grocery store, despite my aesthetic affinity to it.

Digital Supplement to Cash Envelopes

Again, shit happens. Sometimes you will need to use a credit card. Plus if the cash envelopes system goes to plan, I’ll be paying down my credit card balance and want to keep track of anything unforeseen that’s biting me in the ass. That’s why I use Rocket Money (which is an excellent use of $9.80 per month). Basically I supplement the cash envelopes system with Rocket Money to monitor subscriptions, identify anything bogus, and keep track of my combined credit card balance.

In addition, I’ve committed to only using one credit card for “shit happens” spending so that I can more easily monitor that via Rocket Money.

I will keep you posted as I wander further into the cash envelopes wilderness. Have experience with this tactic? Let us know how it’s going!